Identity Must Be Open in the Stablecoin Economy

Download File

Download FileIdentity Must Be Open in the Stablecoin Economy

Arming the rebels in the fight over identity

Stablecoins will succeed. The question is not if, but how. Will they become the foundation of an open financial system anchored by portable identity — or will they harden into closed oligopolies that repeat Web2’s mistakes?

When Facebook bought Instagram for $1 billion, it signaled the dawn of a winner-take-all era. Stripe’s recent $1 billion acquisition of Bridge reminds us that history rhymes: the infrastructure has matured, the market is heating up, and the battle for control of the next financial stack has begun.

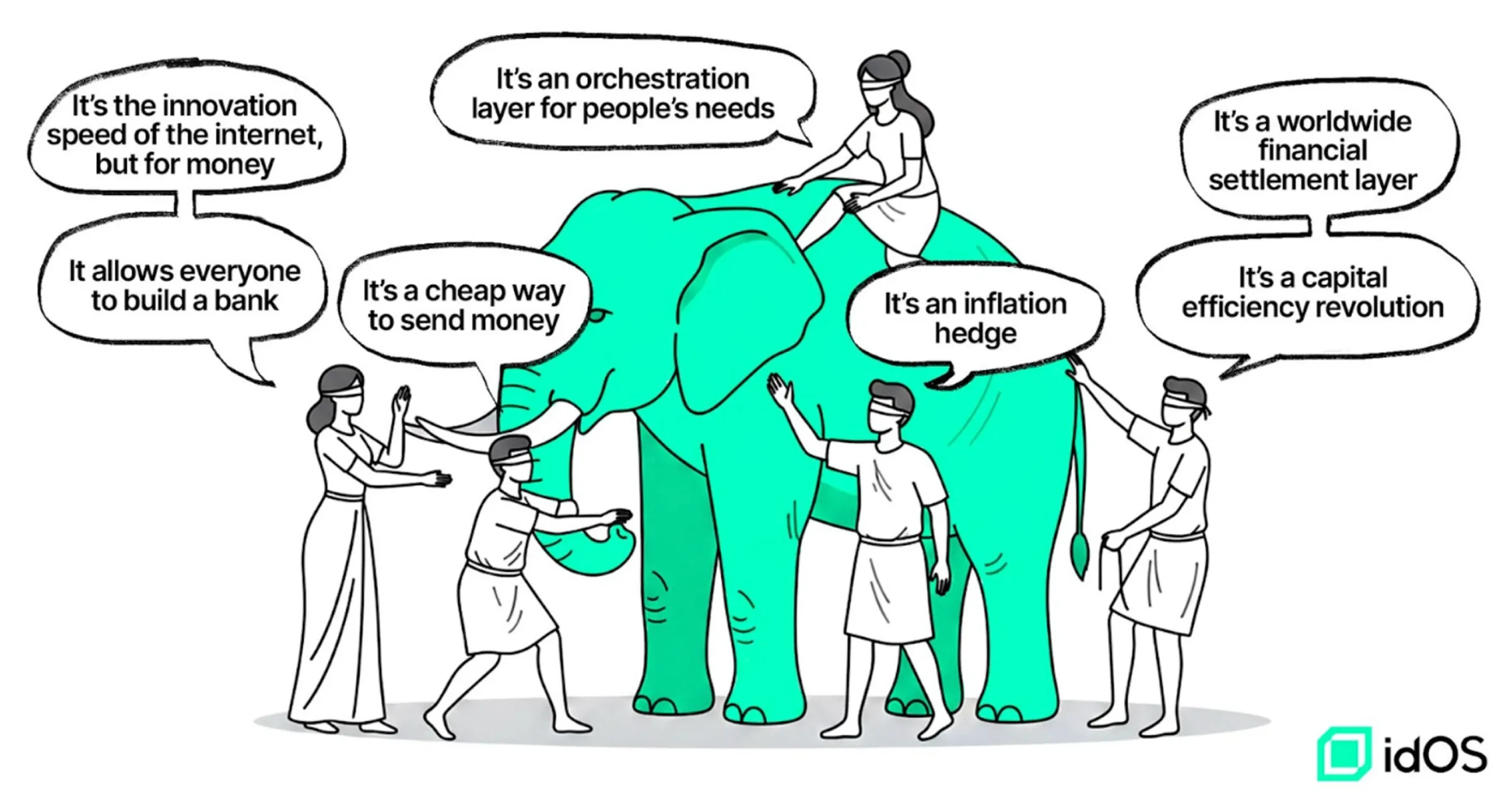

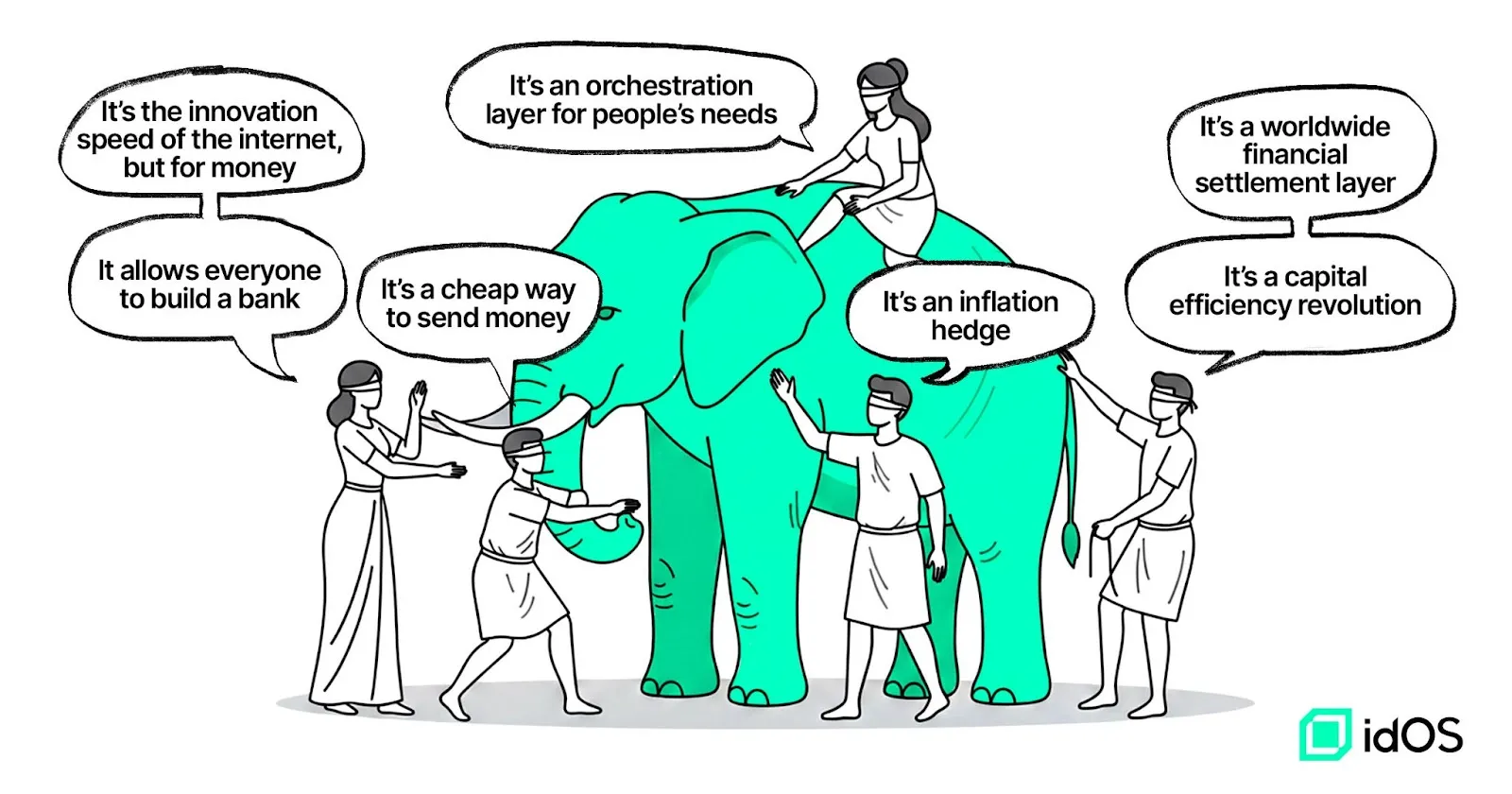

Stablecoins are more than another fintech feature. They are a new substrate for money and markets, colliding head-on with legacy rails that still run on pre-90s infrastructure. Experts we spoke to – like Plasma’s CEO Paul, Nikola VP Payments at TON among others – describe them in many ways: cheap cross-border payments, inflation hedge, programmable savings, capital efficiency, regulatory settlement layer. As in the classic tale of the blind men describing the elephant, they are all right. Stablecoins are all of these things at once.

But there is one part of the elephant almost everyone overlooks: identity. Every serious use case — from remittances to credit, from neobanks to marketplaces — eventually collides with the same question: who is the user? In social media, the chokepoint of identity was captured by a handful of platforms. Walled gardens won, and innovation stalled.

Fixing the tracks to stay open is not some nostalgic dream of early internet idealists — it’s a smart and plain business decision. In social media, only a handful became oligarchs; everyone else was trapped on their platforms. In the stablecoin economy, the smart banks, fintechs, and crypto-native neobanks will learn from the past and avoid platform risks.

Adopting open standards alone is not enough. The real task is to spot the chokepoint and fix it open. And just as in social media, the chokepoint is identity. Which path we take now will define whether stablecoins become another closed empire — or the foundation of an open internet of money.

Bigger than you think it is

Let’s start with the basics: What is this stablecoin economy? Spoiler alert: Ask five blind people and you will get five (or more) answers. A remittance startup CEO sees the massively lower transaction cost stablecoins enable. Neobanks love the ability for their users to switch in and out of currencies that are more stable than their home market’s currencies. These are some of the most prominent features of stablecoins today. And indeed neobanks using stablecoin rails are seeing their highest adoption rates in developing economies.

But there is more.

Another advantage that is already clearly visible today is capital efficiency which DeFi innovation brought us and that has hardened over the last cycles. Its programmatic nature allows for rapid capital formation and capital redistribution. This effectively led to an international financial lingua franca and singular worldwide capital market for nerds.

Stablecoin native neobanks have started entering the arena. This new breed of neobanks completely operate on stablecoin infrastructure, stacking interoperable financial modules like remittances, cards, savings products and even full bank accounts together like Lego bricks. This allows them to operate without a license for a fraction of their fintech competitor’s cost. In addition the cost of entry is plummeting: It used to cost millions to acquire a banking license, now adding fintech features require setup fees in the thousands. At the same time the addressable market expands and time to market shortens drastically for new ‘stablecoin fintechs’. For example, stablecoin-based startups offer an out-of-the-box debit card offering available throughout multiple continents with an implementation time of weeks. The result is more competition from digital native, lean and international entrants.

The following points are less obvious now, but will have a bigger impact down the road.

Because of the open source properties of the stablecoin economy, we will see increased product diversity and even completely new product types that we can’t think of now. People imagined sharing dinner recipes, they didn’t predict memes and reels. The innovation will be driven due to lower cost as well, which will allow for use cases previously not worth pursuing, e.g. – an all time favorite in crypto – micro payments, or agents auto-tipping.

Increasing competition, mixed with cheap infrastructure and interoperable tools, will not just rapidly increase the speed of innovation cycles in finance, it will keep them accelerating. This property of the stablecoin economy will have the biggest impact of them all and it's the reason why we believe open source will prevail. The compounding effects of open source are just too strong to effectively fight.

Banking and fintech with their monolithic approach and limited interoperability enabled a mostly static exchange between the user and the financial product. We envision a financial system that is far more dynamic, built on stablecoin rails that match human needs and wants with the best available goods and services. The stablecoin economy will be a people-centered intent orchestration layer between their needs, their assets and the services and goods waiting for a buyer.

The stablecoin economy isn’t just one of these features, it is all of them at the same time. It’s a typical ‘disruptive technology’ that has the potential to change the way finance works worldwide.

The Digital Identity Explosion

On the internet we progressed from browsers, to profiles and now to wallets. It went from this niche nerdy place that didn’t know identity, to a place that defines our identity, and now a place where we open bank accounts and send money. Stablecoin adoption means that these wallets need to bridge to the real world to enable mass adoption, and that bridge is the real world identity.

Identity is a spectrum: A user can simply create an address using a self-custodial wallet and then use any type of decentralized finance application that he or she likes. The stablecoin economy however, is about going further and offering products that we can use in (what we in the industry strikingly call) the real world. Dabbling with funny internet money is one thing, offering real bank products is another – at least that’s how most regulators see it, and so real-world regulations apply. The most frictionful of them is that anyone offering financial products must prove they know their customers (KYC). This is only a tiny subset of identity, but it is arguably the most annoying for users, inefficient in achieving their goal and come with collateral damage. What is undebatable is that without making KYC work, we will not see a stablecoin economy adoption and will be stuck with the old rails.

At every point along the customer journey and the value chain of the stablecoin fintech stack, you will find the KYC problem. Unlike monolithic banks, stablecoin neobanks mix and match multiple regulated services like on-/off-ramping, virtual IBAN accounts, and crypto cards, and that problem is multiplied across many regulated entities and KYC identity verification providers, creating unnecessary user friction and unnecessary copies of user data stored in centralized honeypots. Current centralized approaches are inadequate. Whether it’s providers sharing user data via dedicated APIs or a centralized company storing and reusing KYC information, neither model solves the business problem of universal identity interoperability and orchestration. Verified users are trapped behind siloed implementations and used as a rent-seeking chokepoint for composability, as we can see with the fintech industry’s struggle with traditional banks over the openness of user data and lawsuits against predatory facilitators playing the platform game. The identity problem is big, and it’s only getting bigger.

As the stablecoin economy takes off, we are going to see three key factors driving an explosion of demand for portable identity that is open, programmatic, and data-minimizing, with the volume of identity verifications needed for compliance increasing as fast as the stablecoin volume itself.

- The first is the most fundamental innovation of web3: the rise of the wallet-delimited web. Wallets are the atomic unit of identity in crypto - and they fully follow the crypto ethos: programmable, disposable, commoditized, secure. Spinning up a new account is no longer a process of applying at the bank or authenticating with Apple and Google (although we’ve back-ported these onto wallets), it’s just simple math. With the rise and commoditization of wallet-as-a-service products, users, businesses and AI agents are all being granted a wallet, oftentimes multiple ones. The wallet address connected to an app is the new CRM, the new direct customer relationship, one which is trusted, cryptographically verifiable and flexible for use as a simple identifier to holding the entire state of a user’s account and transaction history. Wallets let a user transact, mutate public and private state in decentralized applications in an authenticated way, receive and store assets, and more.

- The second is the proliferation of stablecoins themselves - banks, trading firms, fintechs and even retailers are going to start issuing and accepting stablecoins, all stablecoin minting and supply charts are up and to the right. Noncustodial wallets and stablecoins give us programmable bank accounts, and they will, like the embedded finance wave of fintech in web2, end up in every nook and cranny of the economy, everywhere where friction is eliminated, and everywhere where idle value can be turned into margin. As innovations in interoperability and liquidity compound, the traditional centralizing forces of “winner take all” may be kept at bay, as everyone not only wants a piece of the stablecoin margin pie and the control that issuing their own gives them, but also because DeFi rails are flexible enough to accommodate a massive long tail of assets. There will be “true” stablecoins backed by fiat, “yieldcoins” that are really stablecoin-denominated structured products, GPU or resource-backed stablecoins, “flatcoins” and stablecoins for every forex pair on earth.

- The final factor is the inherent composability of stablecoins and the crypto rails they run on. Stablecoins are not a monolithic, “one-and-done” solution - they’re a building block, with well-defined interfaces through things like the ERC-20 or SPL token standards, and they enable you to build more and more complex systems and offer more and more value to customers. We are beginning to see this today with crypto wallets and neobanks offering multiple fiat onramp and centralized exchange services, as well as crypto card programs and embedded bank account payments rolled into a single application. All of these products have entirely different “offchain” components, but all speak the same “onchain” language of stablecoins to interoperate with one another. The USDC you on-ramp can be sent to a bank account or spent in your card, or even deposited into a yield-bearing noncustodial savings account.

That means that exchange relations mediated by stablecoins will explode. Just like we went from having a handful of accounts on the internet to having 200 accounts. In crypto, wallet-delimited web, we will go from having a handful of fintech accounts to having 200.

The crypto industry is coming out of its infancy and making its way up the stack to true consumer-and business-facing applications. As a result, the number of offchain and onchain modules available for builders to orchestrate and compose together to build something new will keep increasing.

Think about a decentralized Angies List labor classifieds app, complete with stablecoin payments, an onchain DAO managed by a dual assembly of one-person-one-vote customers and workers, identity verifications and background checks for workers, distributed dispute resolution via onchain conflict settlement courts, and on and offramps in every country on earth, with un-withdrawn salaries earning interest in Aave. You might even have under-collateralized onchain loans based on onchain salary history and offchain banking data.

This gets even crazier as we start delegating much of our economic life to agents who act on our behalf, doing business amongst themselves, settling in crypto or fiat or both, working with centralized APIs and decentralized services alike. Composability is crypto’s superpower, and the simple “stablecoin Venmo” app is just the beginning for stablecoins penetrating every aspect of the economy.

While we are bullish on a fully cypherpunk “nuke-proof” crypto economy with fully decentralized stablecoins and anonymous payments, evolving alongside that “true believer” defi will be likely a 100x bigger version of crypto that touches every aspect of our financial and commercial lives, necessarily anchoring it to the real world. The real world does not speak wallets, ERC-20 tokens, or permissionless smart contracts. There are roots of trust, there are necessary boundaries for society to coordinate and regulate activity, and these will all involve asking the question “Who are you?” The answer to that question far exceeds a simple KYC process.

What we are arguing is, that this new stablecoin economy can’t possibly work without a smooth, private, interoperable and portable identity solution. Without this, stablecoins will not cross into the mainstream - UX will become too cumbersome for normal users and building great products that rely on identity will be too risky for builders.

We are on the verge of seeing the internet being applied to money at scale, and as a result we see the number of composable relationships between these new modules develop exponentially, just like we had an explosion of online accounts in web2.

Looking back to see the path ahead

Talking about the early internet. Let’s take a look back to the mid-2000s as it will help us understand how this rampant stablecoin economy will evolve. The dotcom bubble had just burst. The Webvans and Pets.com of the late 90s hadn’t prevailed, and funding went from abundant to scarce. The skeptics – laughed at for being dinosaurs during the frenzy – turned out to be right. Supposedly, the world wasn’t drastically changing after all, or so it seemed.

Prelude: What the dotcom boom did, however, was to create massive server overcapacity, making them cheap and reliable. Internet penetration increased and it trained a talent force that stuck around. Even though most companies did not survive, it did provide fertile ground for the next batch. That next batch were social media companies that we call web2 that rule the internet today. The same happened in DeFi: Hacks hardened the infrastructure, node provisioning became commoditized and gas cost came down, talent joined the industry and users started to populate the space. The early days provided the fertile ground that the next batch – the stablecoin economy – is starting out with.

Competitive Landscape: Social media hit mostly national and local media markets. Suddenly, online news spread quickly, the cost of distribution dwindled, and the barrier to entry disappeared for new contenders. This resulted in a bloodbath for formerly high-margin pampered outlets; the ocean turned very red. Newspapers didn’t see the honey trap, that massive reach on social media was to their ability to capture value. Stablecoin contenders will turn the financial market for retail products into a red ocean – a brutally competitive market where incumbents (locally entrenched, running on decade-old infrastructure) are an easy prey for fast-moving competitors on stablecoin rails. That is a good thing for consumers and innovation in general as it forces cheap prices, better products, and quicker innovation cycles.

Formation Phase: Before the pendulum reaches its equilibrium, the swings can be very wild. In the case of social media, the first swing was towards the emergence of national champions who held sway in a particular country or region. In Germany, StudiVZ was that national champion, and early on was rumored to have been offered a 10% stake in Facebook, which it declined, thinking it had a lock on the valuable German market. In Spain Tuenti ‘won’ the race, in Brazil Orkut dominated (launched by Google), Hi5 was popular in Mexico, you get the idea.

Looking at stablecoins today, we see something similar developing in the stablecoin issuance, application, and infrastructure spaces with regional contenders like Société Générale or Deutsche Bank’s subsidiary DWS launching stablecoins, UnionBank launching PHX, JPMorgan launching JPMCoin, etc. There are stablecoins specifically with RWA yield, some for emerging markets, some that are programmatic, some that are especially compliant. Expansion was as inevitable as its contraction. We will see lots of local winners, until they lose against the handful of winners that prevail globally.

Market equilibria: This process has already started: Just like the purchase of Instagram for $1bn by Facebook, Bridge was acquired by Stripe for – you guessed it – $1bn. The reason that early winners in the social media war began aggressively purchasing companies was that they understood the network effects involved and the equilibrium of the market once the dust settles. They understood that the winner would not take away one market ,but all of them (the markets not heavily protected like the Chinese market).

The early internet promised everyone a level playing field, but open standards don’t guarantee open outcomes. Even though social media made use of these open standards, from HTTP to HTML to SMTP, it closed the choke point – the social graph. Competing products could be amazing, but without your friends around it didn’t matter. The ones that did show early signs of traction were aggressively bought out. The products that had something to offer were purchased to make the walled garden even greener – and the walls even higher.

Platform Risks: Building on proprietary platforms carries existential risks as Meerkat, a video streaming platform on Twitter, experienced. Building an overnight success app, they used Twitter’s distribution to gain users which they rapidly did. Meerkat’s API access to Twitter was shut down the same year it launched and Twitter instead acquired and promoted its own clone. The message was clear and everyone building their audience on Facebook and Twitter questions if they had made a big mistake bringing their users into someone else’s walled garden.

When the playbook failed to work and Mark Zuckerberg found himself unable to buy Snapchat that was hugely popular with young users, he set an example and made sure others heard the message. Instagram looked like Snapchat in a matter of weeks. The message was clear again: dare to compete and we will do everything possible to make sure you will fail. Today Facebook is 155 times more valuable than Snapchat. The winner took it all.

Aftermath: The internet we have today theoretically allows for competition. his is why regulators worldwide had a hard time reacting to anticompetitive behaviour. There is still an abundance of sites. But still we ended up with what feels like the entire internet living inside Facebook.

We can even feel those lock in effects: who hasn’t recognized that using social media made them envious, addicted or raging? Social media is like the vampire finch that draws just as much blood that bigger birds don’t bother. We don’t bother changing, because there are no options. It’s just about good enough.

Our town square, the place that impacts relationships, our everyday lives and even elections are in the hand of a few people that have no obligation or incentive to make it work well for us – their users — or society as a whole really.

We will not know anytime soon how social media could in fact feel amazing, where users could easily switch between plenty of highly competitive alternatives that all compete to make their lives better. Where algorithms are transparent and governance of these platforms is done in a way we long ago decided we want to run society: democratically.

Open standards don’t guarantee an open future. It’s on us to identify the choke points to make sure they stay open.

Open source won before (and it can win again)

The good news is that open source can win. We are so certain because it has won before.

As we like to say in crypto—we are early. Early enough in the adoption lifecycle that the market topology under mass adoption is not yet set; the future is still unwritten. When IBM committed $1bn to Linux in 2000, it wasn’t a bet on a single product—it was a bet on a neutral, shared substrate that allowed an entire ecosystem to compound. That choice helped shift the world from proprietary UNIX silos to a commons where vendors competed on quality and innovation, not lock-in.

We see the need for identity taking an open, decentralized public-goods shape—closer to Linux. Treating real-world identity as a composable protocol, not a rent-seeking, closed implementation, makes sense not only for crypto ethos but is a hard business necessity for consumer crypto-fintechs that don’t want to end up like Meerkat did. An open, permissionless stack lets applications and financial services monetize their value-add in a privacy-preserving way—cooperating programmatically instead of hoarding identity data behind closed walls and extractive APIs (if any). Apps can reduce each other’s onboarding friction and enable higher-order aggregation of services suitable for web2-grade experiences or personal financial AI agents. Standards for biometrics, interoperable KYC schemas, and new network features can be set by decentralized governance rather than a single company’s roadmap.

If the Linux Kernel proved that open protocols can out-innovate closed incumbents, idOS - the Identity Operating System - can be that protocol for identity: a neutral, composable layer where value accrues to builders and users—not gatekeepers. Choosing openness now prevents tomorrow’s identity enclosure movement and unlocks the compounding network effects that the next generation of consumer crypto and fintech will depend on.

Identity must be open in the stablecoin economy

Identity stands at a familiar fork in the road: either we repeat the walled-garden playbook, or we commit to a commons for identity. Under closed, proprietary identity, price discovery is broken. Early winners can extract excess rents—if they grant access at all—while smaller providers onboarding valuable niches have no way to monetize their work, leaving identity as a pure cost center.

As it was clear to IBM when they bet big on Linux, we think it will become clear to stablecoin applications, neobanks and crypto fintechs that adopting an open identity stack will represent much more than just an ideological nicety - it is a critical business imperative. Building a business on closed platforms for something as crucial as identity is like building a house on a foundation of sand. As we saw with the lawsuit against Plaid’s commercial use of customer data (and ironically enough as we are seeing with Plaid’s own struggle to preserve open access to underlying account information), identity data in fintech is so valuable that businesses can quickly lose their leverage if it is turned into a centralized provider’s moat.

With an open identity economy, builders get that leverage back. Portability and user agency come by default; vendor risk is minimized through core components run by a decentralized protocol that you can fork; compliance primitives are auditable and verifiable on shared rails; reusable credentials lower CAC across the industry; privacy is strengthened through selective disclosure; resilience comes from a distributed operator set; and developer velocity accelerates through standard interfaces.

With idOS, we see a path to turn identity from a chokepoint for rent extraction into an open economy where participants are paid for issuing data into a privacy-preserving “data commons,” while users retain sovereignty. That dynamic should foster industry-wide cooperation to lower customer acquisition costs for everyone, and shift competition toward building better products rather than taxing scale. It reduces duplication of effort, time, and cost on all sides, and brings onboarding for regulated parts of the stablecoin economy closer to the frictionlessness of the underlying blockchain rails.

In idOS, beyond end users, the two primary market participants are data issuers and data consumers. Any party can issue data on a user’s behalf to their idOS profile as a W3C Verifiable Credential and set a price for reuse. In practice, issuers will typically be regulated obliged entities (OEs) at the crypto–real-world interface—on-ramps, card issuers, embedded bank-account providers, and similar. The issuer’s cryptographic “stamp” confers trust for those willing to rely on it, mirroring a legal concept many already use: reliance. idOS protocolizes this via passporting—off-chain circles of trust represented on-chain. Within a passporting club, issuers can price credential reuse through an Access Grant fee that a consumer pays (with user consent via signature) to reuse the data.

We also recognize passporting will take time to spread and may not fit every jurisdiction or banking partner. As an alternative, idOS supports an ingestion model—where a consumer buys access to the underlying data and runs its own programmatic KYC checks, instead of recollecting everything from scratch.

idOS exposes a protocol for a market to form amongst users, data issuers, data consumers, and applications. Users get one-click, privacy-preserving, self-custodial onboarding (and can share in access-grant revenue if an issuer chooses). Applications lower customer acquisition cost and can increase average revenue per user by upselling additional services—cards, bank accounts, and more—with minimal friction. Regulated parties can both monetize the data they produce and pay a nominal fee to acquire a high-intent user without re-KYC churn. Incentives align. Much has been promised about a “data economy” where users are paid for their data; identity in the stablecoin economy is a concrete, compliance-compatible place to start building that reality.

Choosing the open path

Stablecoin startups are raising tens of millions of dollars, the total stablecoin market capitalization is up and to the right, and mainstream players from web2 and traditional fintech are taking notice. We are at a critical inflection point in the development of these new open financial rails. We can let the critical user identity chokepoint centralize to the point of negating the very benefits of open stablecoin finance on blockchain rails, and end up with a crypto stack that looks like Facebook, or we can build an open protocol that allows for maximum cooperation, competition, and ultimately, innovation - much like Linux.

We see a world of local players emerging and thriving on an open stack, and innovative new applications being able to bootstrap their onboarding process by plugging into the idOS data commons, enabling not just the proliferation of payments and basic neobanking services, but even higher order innovative products, like gig marketplaces which require identify verification of service providers and customers, stablecoin e-commerce protocols which want a global reach but local compliance, and so much more.

We’re bullish on idOS because everywhere we see stablecoins going, we see the identity problem not only appearing, but multiplying. As the industry matures and products need to compose across chains, applications, fintech providers, and asset issuers, we see the idOS network as providing the crucial identity glue to make the whole value chain work together.

So it’s time to choose. Will we allow the market to consolidate around a few major centralized players hoarding user data for themselves, or will we arm the rebels?

--

Ben Basche is the Chief Product Officer at idOS, where he drives product strategy at the intersection of stablecoins, digital identity, and open financial infrastructure. Before idOS, he worked at Rainbow and consulted for projects like Uniswap, Privy and Ready. Ben wrote one of the first articles on the stablecoin economy in 2023 which is how he met Julian.

Julian Leitloff is the co-founder and CEO of idOS, the open identity layer for the stablecoin economy. He has been working on decentralized identity in web3 since 2017. He wrote an early piece on the OpenFi movement. Julian started his career at Deutsche Bank before doing research on early crowdfunding which brought him into crypto.